This week we saw two major deals in the ADC landscape of oncology:

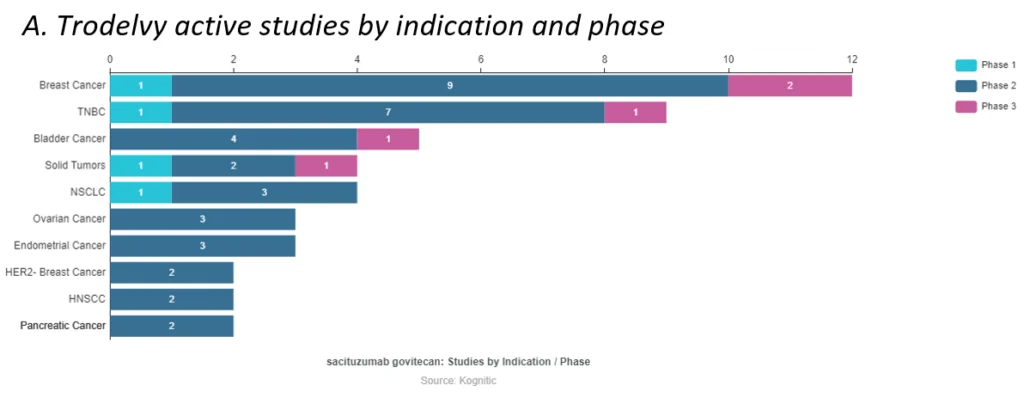

Gilead acquired Immunomedic’s Trop2-directed Trodelvy in a $21B deal, giving the company a footing in the solid tumor space (see infographic A). Already having a strong presence in blood cancer from the Kite Pharma acquisition, Gilead’s portfolio now stands strongly across clinical oncology.

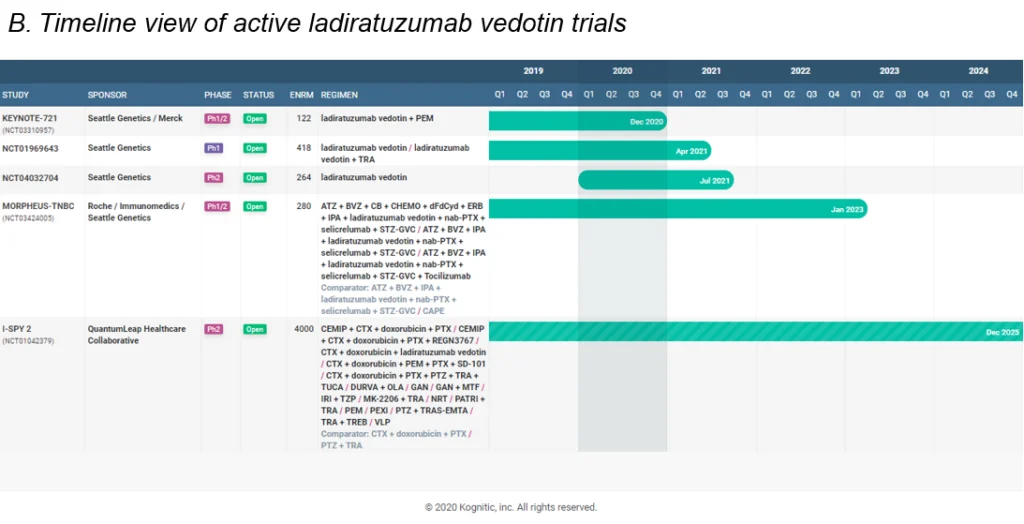

Now Merck and Seattle Genetics have partnered to develop SGN’s ADC drug – ladiratuzumab vedotin in a $1.6B deal. The drug currently has 5 active studies (see infographic B), with Merck intending to next explore it in combination with their own pembrolizumab. Another pact allows Merck to market Tukysa outside the US.

Other happenings in the ADC space in these last few days:

Additionally, Merck KGAA is investing in the expansion of their ADC manufacturing facility.

As Exelisis looks to broaden their pipeline beyond Cabozantinib, they partnered with NBE to leverage their ADC platform technology in developing novel ADC candidates. Exelsis will make an upfront payment of $25M in return for an exclusive option for a set number of targets on NBE-ADC platform over 2 years.

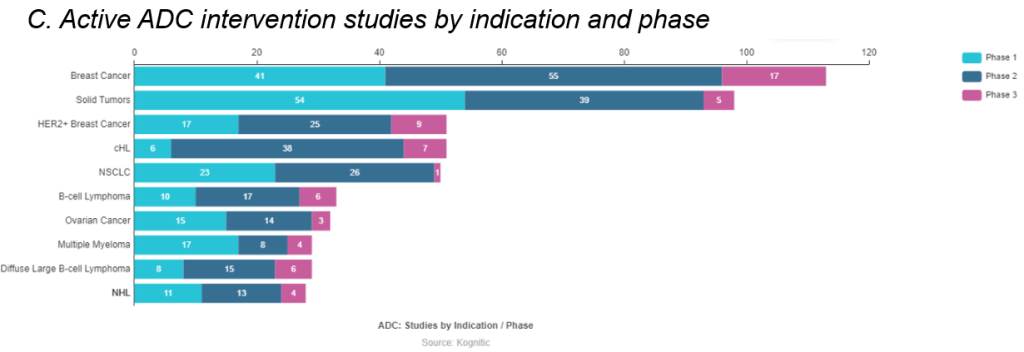

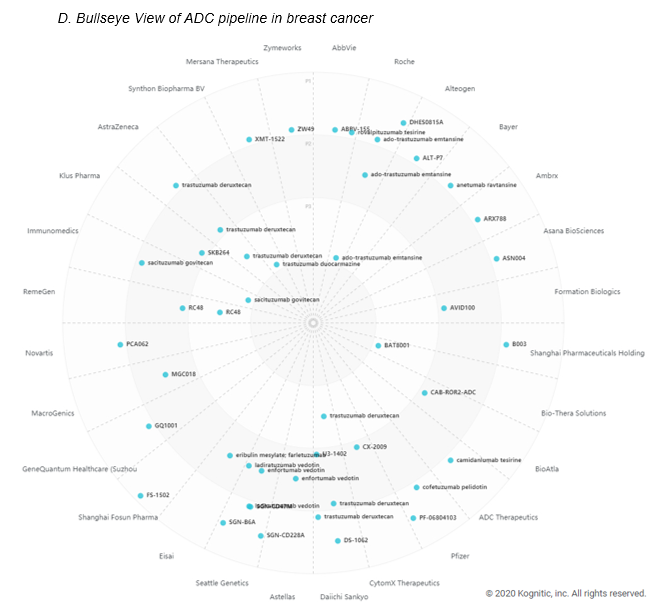

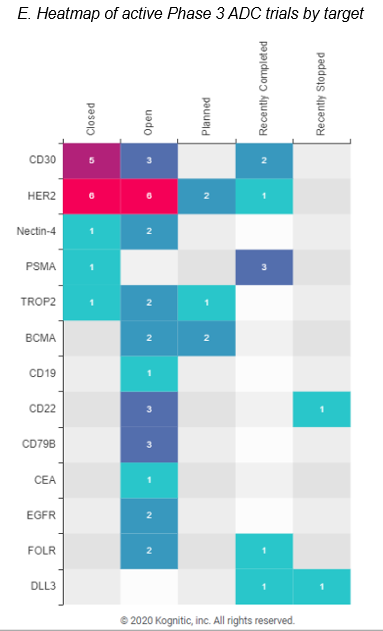

ADCs are projected to be worth 15 billion dollars by 2030. ADCs, or antibody-drug conjugates, are composed of an antibody attached via a linker to a cytotoxic drug (e.g. chemotherapy drugs). Interest in the modality has been in flux until companies got the constructs right. The complexity in getting a right ADC lies in choosing the right target tumor antigen, linker design, conjugation chemistry, drug payload. AstraZeneca/Daiichi’s collaborative commercialization deals for 2 drugs – Enhetru and DS-1062 – has strengthened this ADC space and now ten ADCs have been thus far approved. ADCs drugs are being explored greatly in breast cancer and solid tumors studies (see infographic C and D) with a variety of drug targets (see infographic E).

For a detailed, competitive analysis of the ADC landscape, please reach out to info@kognitic.com